Please, pretty please ...

As the clock hands ticked around past midnight earlier this week, March 31 sliding into April 1, the business world moved from the first to second quarters of this extraordinary year. Thanks to the coronavirus, it’s been a first three months unlike pretty much anything in global economic history. And as the business sage Warren Buffet once observed, ‘Only when the tide goes out do you discover who's been swimming naked.’

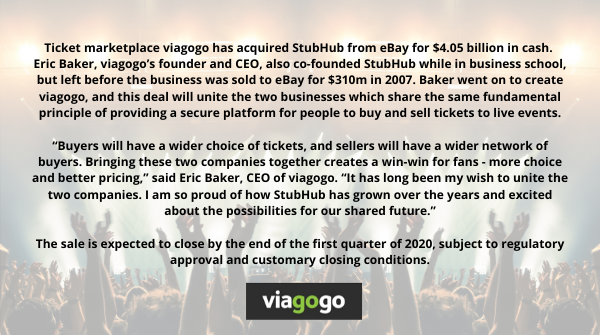

Buffet’s caution about getting caught au naturel is why legitimate questions are starting to increase about whether or not secondary ticket channel Viagogo will be able to close on their USD4.05 billion all-cash purchase of rivals StubHub.

The deal, which sees Viagogo take on approximately USD2 billion in debt, was announced in November last year with the pledge that – subject to regulatory approval – the acquisition would be closed by the end of 1Q 2020.

If March 31 was a reasonable deadline five months ago, pre-coronavirus, it seems ludicrous now in today’s safety-first investing environment. Especially as StubHub is actually the bigger of the two entities.

Sports Illustrated’s John Wall Street column reported last Friday about M&A activity across the sport-tech industry: ‘as long as the economy remains in flux and the sports world is on hiatus, sports-related investments and M&A activity will be limited.’And as DAIMANI suggested last week, in a report on StubHub getting slapped down by the UK advertising regulator for the third time in only three months, there was already sentiment in the US that Baker had overpaid, and that was before coronavirus:

‘One source suggested "Eric Baker and co. have likely realized they're paying +/- $1 billion too much (they paid 25x EBITDA) and now need to slash salaries to make the debits and credits more palatable." While the deal is expected to close, it may not happen as ‘swiftly’ as one might expect an all-cash pact to; we've heard that Viagogo has been shopping minority stakes.’

In fact in January this year, the Moody’s rating agency downgraded to B2 the corporate family rating of PUG LLC [Pugnacious Endeavors Inc, the Delaware-registered entity that is Viagogo]. That rating’s advice was reaffirmed at the end of last month, with the company’s outlook changed from stable to negative.

The full PUG LLC analysis is available behind the Moody’s registration wall here.This was Moody’s sober assessment:

‘Notwithstanding the relatively high equity contribution to the USD4 billion [StubHub] purchase price (i.e. more than 50% will be funded with new common and preferred equity), we view Viagogo's financial policies to be aggressive reflected by its decision to increase financial leverage at closing by one turn to the mid 5 times range. The company indicates it is focused on rapid improvement in leverage, but debt agreements include proposed terms that allow total leverage to increase above closing levels. Concentrated voting control, lack of public financial disclosure, and the absence of board independence weigh on the credit profile.’

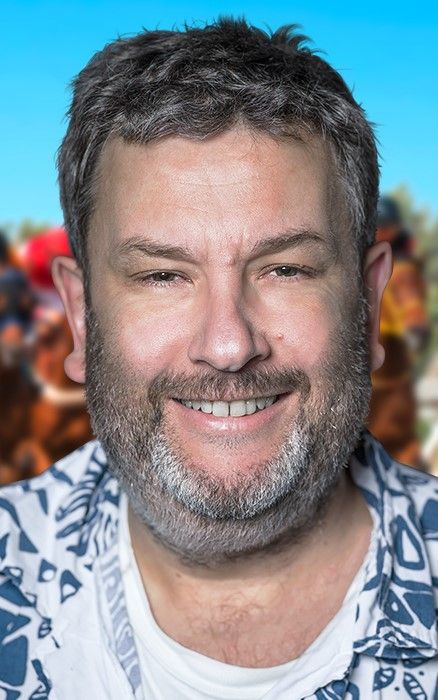

This is Viagogo’s Eric Baker, on CNBC, talking up the Stubagogo deal. The timing of the CNBC interview is significant here – February 21 – which was some time before the true ‘global’ extent of the coronavirus impact was clear. In fact, Baker bats off questions from CNBC about the coronavirus saying the live events affected are mainly in China, Taiwan and Singapore.

‘It was a bit puzzling to hear the company state that "We firmly believe in the StubHub business, and we are excited about its future growth potential with Viagogo as its owner." After all, if there was a lot of growth potential with StubHub, eBay certainly could have used it -- in the past year, its revenue of $10.9 billion is up only modestly up from the prior-year tally of $10.6 billion.’Since the collapse of the Live Event business, both ‘Stubagogo’ companies have got busy involving themselves in the politically fraught and improbable dance of trying to convince Washington that machine-driven ticket-scalping is actually worthy of being included in the federal government’s USD2.2 trillion support package.

Whether both companies can secure some form of government relief may prove crucial from a reputational point of view, as customers of both platforms have remained noisily unimpressed when trying to get refunds for events that have been either cancelled or postponed off into the far-distance.

Why is DAIMANI even interested in this? After all neither company offer the same sort of official VIP hospitality access that we do.

Well, we’ve been following this merger closely because both companies have a truly wretched record. And anything that is bad for the Live Event business is, ultimately, bad for all of us.

It’s not saying much but Viagogo’s reputation is worse than StubHub, but both consistently bring great discredit to those of us in the Live Event business trying to make sure that customers are not short changed with exorbitant markups, hidden fees, and get what they pay for.

Legendary Italian Live Event promoter Claudio Trotta, who heads Barley Arts, put the ‘Stubagogo’ merger plan into some context when he wrote earlier this week:‘When I received word of Viagogo’s plans to acquire StubHub, it was one of the worst pieces of news I had received in my more than 40 years in the business.

‘First of all, the fact that Viagogo can spend USD4 billion in cash is very worrying. Secondly, that Viagogo has bought a competitor that operates in most countries means we are still really far from winning the battle against this cancer – and I do truly believe it is a cancer – which has been eating away at the live music industry for far too long now.’ [our emphases]

It’s not a stretch to say that Viagogo is Darth Vader to StubHub’s Anakin Skywalker. Both work on the ‘dark side’ and, in a Star Wars-like twist, actually have the same father: businessman Eric Baker, who co-founded StubHub in 2000 then sold it to eBay seven years later for USD310 million, before founding Viagogo in 2006.

Needless to say Baker has been trilling enthusiastically about how exciting ‘Stubagogo’ will be for customers:

‘Buyers will have a wider choice of tickets, and sellers will have a wider network of buyers. Bringing these two companies together creates a win-win for fans - more choice and better pricing.’

However, Baker’s announcement on Viagogo’s official Twitter site allowed customers to give vent to their true feelings:

Hope not . You’re a shocking company . Done me for nearly one thousand pounds for 2 concert tickets costing less than two hundred quid . And then ignored me . Buyers beware !!

— Mike Osmond (@mikeosmond) November 25, 2019

And neither was the CEO of StubHub spared when she announced her company’s sale to Viagogo:

Scalping. It's called scalping.

— asif khan (@oobivat) November 25, 2019

An added wrinkle to Stubagogo is the threat posed by regulatory action. As soon as the ‘Stubagogo’ plans were announced the UK government’s Competition and Markets Authority opened an investigation, asking for comments from the industry and public.

The deadline for comments was January 10 but the fact so many government offices are now closed may mean a delayed response from the CMA is likely.

Even so, in these coronavirus times, Viagogo has become something like Typhoid Mary, such a polarising figure that at the minimum some form of restraint, disruption or special measures seems inevitable before Stubagogo gets the UK government’s blessing – if it ever does.

There can’t be too many companies in the world that regularly attract this sort of headlines, from the Guardian: Is Viagogo one of the worst businesses in Britain?